High copper prices can cover a multitude of sins.

But there is a scary trend among the giant copper mines of the world…age and decline.

Mines are like loaves of bread in a sandwich shop. When the bread runs out, you start a new batch. And right now, we have a lot of mines coming to the end of their lives.

That’s why mining companies need to be on the lookout for their next mine. The problem for the copper industry is a handful of absolute geologic monstrosities that are coming to an end.

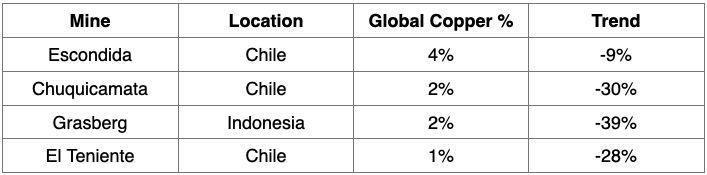

Here’s an example of some of the world’s largest copper mines and their production trend:

Chuquicamata, Grasberg and El Teniente are old. Grasberg went into production in the 1970’s. El Teniente began modern operations in 1912. However, operations there date back to 1819. That’s over 200 years of copper production.

The following giant mines produced for more than 50 years:

- Chuquicamata (Chile, Codelco) – 18th largest copper mine by 2025 production.

- El Teniente (Chile, Codelco) – eighth largest mine in the world. Modern mining began there in 1905.

- Buenavista del Cobre (Mexico, Southern Copper/Grupo México) – fifth largest copper mine in the world. Mining began in 1899.

- Morenci (USA, Freeport McMoRan) – eleventh largest copper mine in the world. Modern mining dates to the 1880s.

- Bingham Canyon / Kennecott (USA, Rio Tinto) – Top 20 largest copper producer in the world. In production since 1906.

These mines will keep producing less copper per ton of rock moved. Higher copper prices will offset some of the grade decline. However, we need more copper, not the same or less.

According to the United Nations Global Trade Update:

Global copper demand is expected to grow by over 40% by 2040, but supply isn’t keeping pace. Meeting this demand may require 80 new mines and $250 billion in investment by 2030.

To be clear, we need more copper. S&P Global analysts project peak copper mined production in 2030 at thirty-three million metric tons. Declining copper supply and increased demand could result in a ten million metric ton shortfall by 2040.

In other words, we need to add 670,000 metric tons of new supply per year for the next fifteen years. That means we need to find, permit, and put into production a new Escondida mine every year.

Ideally, we would have started doing so 20 years ago. But building and permitting new mines has become extremely difficult and expensive.

This means companies with large existing operations, or even projects in development, could see the value of their assets continuing to rise.

This is a signal that copper prices should remain high and could go significantly higher. Existing supply is in decline and demand is rising… that points to higher prices.

Retail investors should hold copper producers in their portfolio. An easy way to get that exposure is by owning Global X Copper Miners ETF (NYSE: COPX).

Miners soared as the copper price hit all-time highs. But this could go much higher.

This will also mean new copper discoveries should rocket higher in value. We’re currently evaluating a number of promising development projects which could profit from this trend for a decade-plus.

More on that soon.