There is a huge disconnect in the mining industry today that could make a lot of people rich. It comes down to math and assumptions.

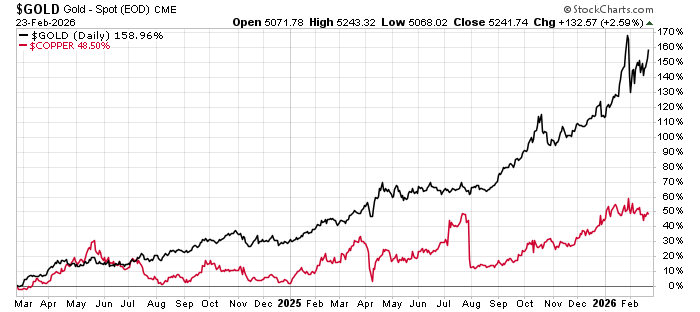

Right now, people look at this chart and think, “I missed it.”

We haven’t missed anything yet. In fact, we need to remember that the stuff these companies produce (in this case gold and copper), did this:

As we can see (if we didn’t already know) copper, gold, and many other metals prices are at all-time highs. Miners are “price takers”. That means they produce the metal, but don’t set the price that they sell it for. With metal prices at all-time highs, these companies are raking in cash. But they aren’t priced that way.

That’s our opportunity. There are a lot of projects out there that are on the verge of production. I wrote about the bad ones in my recent essay.

How do we know what’s bad, and what’s good?

To solve that, we need to know what metal prices to use when we look at existing projects. Historically, acquisitions occur at or slightly below the net asset value of the company (NAV) for advanced projects and producers.

Less advanced or single asset companies have a slightly lower value at around 0.8 times NAV. The mystery is how you determine the actual NAV.

Here’s what I mean…

There’s a company called Snowline Gold (SNWGF), which owns the Valley Project in the Yukon Territory of Canada. Great place to build a mine – safe, lawful, with solid infrastructure. So it should be relatively low jurisdictional risk (that’s where communities/governments steal the asset, change the tax laws, or something similar).

The deposit is robust, with a resource of 7.9 million ounces of gold at 1.2 g/t grade. That’s an economic deposit that can make money at a range of gold prices. The mine itself is a simple truck and shovel plan. It will cost about C$1.7 billion to build, which is quite manageable.

But what investors really need to know is its worth today. That’s why we need to know its NAV.

Snowline’s Valley project has several NAVs associated with it, based on different criteria. However, the most important is the gold price assumption. Here are current NAV calculations on different gold prices:

- C$2.8 billion at a gold price of $2,250 per ounce (2025, CIBC bank)

- C$5.5 billion at a gold price of $3,200 per ounce (2025, CIBC bank)

- C$3.4 billion at a gold price of $2,150 per ounce (2026, company)

- C$10.7 billion at a gold price of $4,300 per ounce (2026, company)

Snowline’s current market value is C$3.0 billion. That means it currently trades at its NAV if the gold price is less than $2,500 per ounce. It trades at less than 0.3 times the NAV at $4,300 per ounce.

So, which one is correct?

If we buy the stock at 1x NAV, we probably won’t make much money. But if we buy it at 0.3x NAV, we could easily double or triple our investment.

That means we need to go back and look at the gold price again.

As we can see, there were three major declines in the gold price over the last 30 years.

- 1988 to 2001: Gold price fell 45%.

- 2008 to 2009: Gold price fell 25%.

- 2011 to 2016: Gold price fell 43%.

In other words, there is some risk of a decline in price. However, the trend remains up today, so we don’t know where the gold price will settle. If we priced in a possible 45% fall from today, the gold price would be $2,880 per ounce.

In the context of Snowline’s NAV, that’s somewhere around C$4.0 billion. So, the current price of Snowline gold is less than 1 times the asset value, if we assume that the gold price will fall 45% from today…

I don’t know about you, but that seems incredibly cheap. And there are many of these projects kicking around. Not just in gold, but silver, copper, nickel, etc.

When we evaluate the NAVs, it’s important to start with strong projects. Then we can figure out the value and invest accordingly.